Related Posts

September 11, 2025

Smart Beta Strategies: What Investors Should Know Before Investing

Smart Beta Strategies: What Investors Should Know Before Investing As of August 2025, Indian mutual…

May 7, 2025

Process Matters More Than Outcome

I have spent nearly a decade of my life trading energy derivatives, and today I…

April 30, 2025

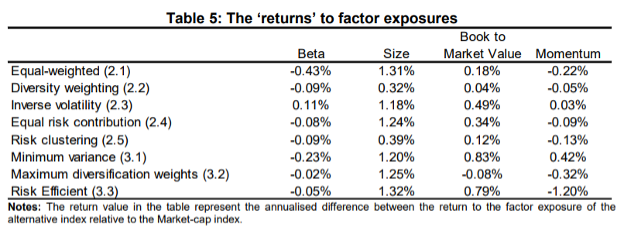

Is Market Cap the Best Way to Build an Index?

Nifty 50 is a free-float weighted index – a slight variation of market cap weighted…

April 23, 2025

3 Books That Changed How I Think About Risk and Markets

Over the past two decades, I’ve built a quiet but consistent habit — reading. Not…