Compound interest is one of the most powerful forces on earth. It can do great things when used to create wealth. Understanding how compound interest works is an indispensable tool for living a wealthy life. This article will show you how to make sure that compound interest is always working in your favor.

Power Of Compounding: The Basics

The definition of compounding interest may seem obvious, but there’s more to this seemingly simple concept than it first appears. This effect of compound interest works both ways. Money left alone in a savings account for even just one year can be developed by compound interest. That is if the account earns at least a minimum amount of interest per year. In this sense, receiving an annual interest rate of 3% on your savings account may be more significant than it seems.

In fact, if you add around Rs 100000 to your savings account (and the money allows for continuous growth over time), then in just one year, you will have earned what looks like a small sum: only Rs 744.250. Yet, that small initial investment will double to become Rs 1488.500 after just two years. But after five years (Rs 3721.250), ten years (Rs 7442.500), fifteen years (Rs 29770.000), or even twenty-five years (Rs 119080.000). That’s the life-changing power of compounding! And all because you let compounding take its natural course, and you didn’t touch the original investment.

This concept of compounding interest over time is what makes it possible to turn a small sum into millions or a small amount of money into an enormous fortune. And this power really becomes apparent when we remember that compound interest actually works best in the long term. That’s because, as a general rule, more time allows for greater profits through compound interest: after ten years, Rs 744.250 will become Rs 2977.000 (a 200% increase), but twenty-five years later, it’ll be worth Rs 119080.000 (a 4000% jump).

Misunderstanding Regarding The Power of Compounding:

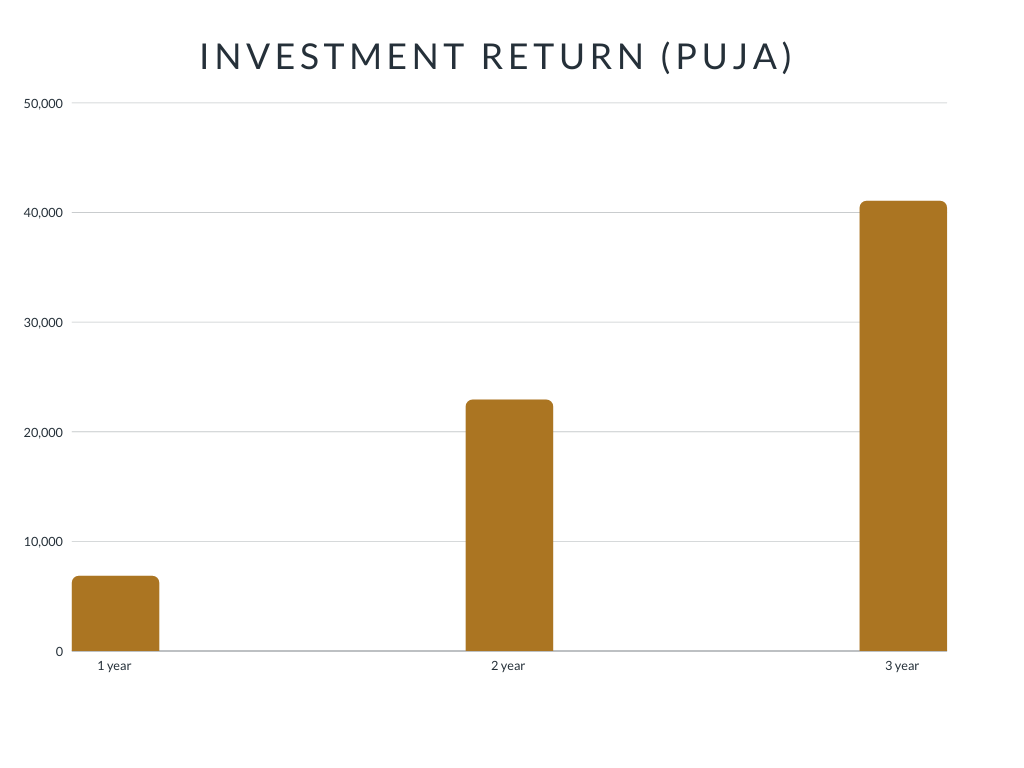

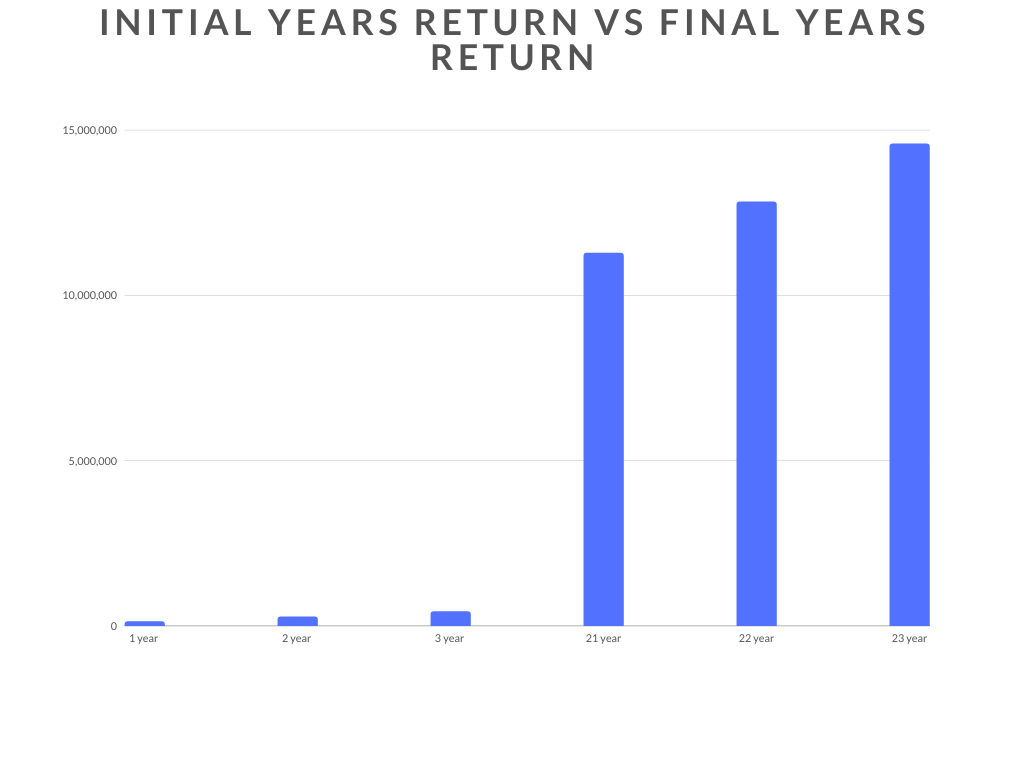

Puja invests INR 10,000 monthly into the stock market starting at age 22 and earns 12% average annual returns each year until age 45.

Kartik invests 15,000 every month and earns 12% average annual returns until age 45. But he doesn’t start investing until he is 30 years old, which makes his total investment amount less than Edgar’s when they both reach the same age.