Why We Built Gear 6A for Mutual Funds — And How It Works

India's mutual fund industry now manages over ₹82 lakh crore. There are 2,500+ schemes across 44 AMCs. And with that many options, we've seen most investors do the same thing. They open App, sort by 1-year returns, and pick whatever's on top.

We've watched this play out multiple times. Majority of the times it backfires.

Here's what we've learned from years of working with investors. The right starting point is never "which fund." It's "where should my money go?" Your goal, your time horizon, your ability to see a 20% drop. That's what should decide allocation. Not what topped the charts last quarter. Short-term money belongs in debt funds. Long-term money can sit in equity. Get this one decision wrong, and it doesn't matter how good your fund picks are.

Most investors pick funds the wrong way. They look at returns and stop there. In our conversations with clients, we keep asking the same question: "Did you check how much risk that fund took to earn those returns?" Almost nobody does. Did it beat its benchmark consistently, or did it just have one great year? How badly did it fall when markets corrected? And then there's cost. Even a 0.3% difference in expense ratio sounds like nothing. Over 15 years, it quietly eats into lakhs.

But the bigger problem isn't buying. It's selling. This is where we've seen investors hurt themselves the most. One bad quarter, and they want out. Markets fall 10%, and they panic-sell. Or they see a friend's fund doing better and switch. That's recency bias doing its thing. And every exit comes with a bill. Most equity funds charge around 1% exit load within a year. Short-term gains are taxed at 20%, long-term gains above ₹1.25 lakh at 12.5%. One poorly timed switch can wipe out a full year of outperformance. We've seen it happen. You need a framework for exits, not a feeling. Review a fund if the manager changes or the strategy drifts meaningfully. But give it time. Don't react to noise.

No chasing. No reacting. Just discipline compounding quietly.

The Core Philosophy

There's no shortage of ways to pick mutual funds. Star ratings. Recent returns. Your neighbour's tip. Your RM's quarterly call. They all share one flaw — they look backwards at the wrong thing.

We believe good fund selection requires a systematic, data-driven approach. Not gut feel. Not star ratings. Not last quarter's topper.

Think of it like hiring a cricket coach based purely on last season's batting average. You'd miss everything that matters — technique, temperament, performance under pressure, recovery from a bad patch. Returns work the same way. The factsheet number is the outcome. We care about the process behind it, and whether that process holds up.

Our methodology rests on three pillars.

- Risk-adjusted performance over raw returns. A fund delivering 20% with massive drawdowns is not the same as one delivering 18% with far lower volatility. The first just looks better on paper. When markets correct — and they always do — the steadier fund is worth more than its headline return suggests. We use Information Ratio and Maximum Drawdown as our primary filters for this reason.

- Medium-term consistency over short-term brilliance. We exclude funds with less than three years of track record. Six months of strong performance tells you almost nothing — it could be luck, a favourable regime, or a concentrated bet that paid off. Three years covers enough market cycles. You see how the fund behaved in rallies, corrections, and the dull stretches between. That's where skill separates from noise.

- Structural diversification over concentrated bets. Any momentum-driven process, left unchecked, gravitates toward whatever works right now. In a mid-cap bull run, you end up overloaded with mid-cap funds. In a quality rally, everything looks like a quality play. That feels great — until the regime changes. And it always changes. Diversification ensures the portfolio never becomes a concentrated bet on the last twelve months.

These three pillars work together. Quality first. Consistency as the filter. Diversification as the guardrail. Remove any one, and you're left with a slightly fancier version of performance chasing.

How It Works

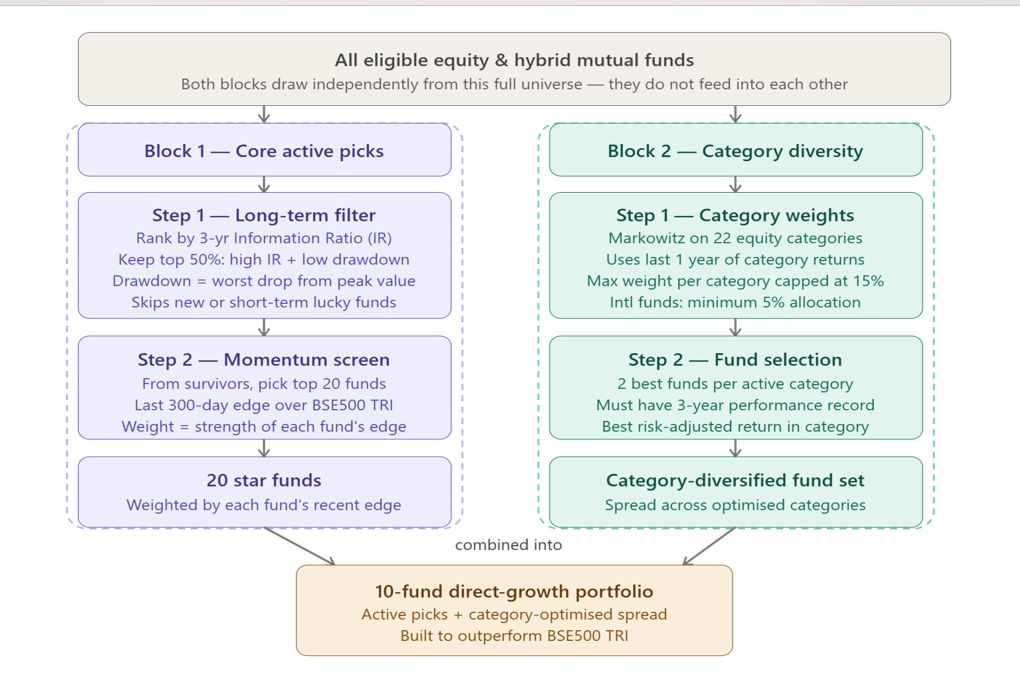

The methodology runs in two blocks. Block 1 is the conviction engine. Block 2 is the diversification guardrail.

Block 1 starts with a quality filter. We take the top half of eligible equity and hybrid funds, ranked by 3-year Information Ratio and Maximum Drawdown relative to category. From that filtered set, we pick the top 20 based on outperformance vs. the BSE 500 TRI over the last 300 trading days.

No. The sequencing matters. We filter first for long-term risk-adjusted quality, then apply momentum. The question is narrow: among funds that have proven themselves over three years, which ones are currently in form? That's very different from chasing last quarter's topper.

Block 2 handles diversification. We assign weights across 22 equity fund categories using Markowitz Optimization. Each category caps at 15%. International funds get a minimum 5% allocation. For each category that receives weight, we pick two funds with at least three years of track record and strong risk-adjusted performance vs. peers.

Block 1 primarily focuses on allocations to large-cap, flexi-cap, and mid-cap categories, while Block 2 is designed to diversify exposure across small-cap, international, value, and other investment segments.

The two blocks combine into a final portfolio of 10 funds.

What the Back-Tests Show

These are back-tested results — not live performance. Simulated returns carry biases and do not guarantee future results.

With that caveat stated clearly:

Lump-sum investors rebalancing every 12 months saw median annual after-tax outperformance vs. the BSE 500 of +3.3%, ranging from +1.3% to +6.3% over three years.

SIP investors saw more modest results — a median ending portfolio value +3.8% above the BSE 500, ranging from 1.3% to 6.4%.

We account for all costs. Most fund selection frameworks quietly ignore this. We don't.

Every rebalance triggers two costs — exit load and capital gains tax. Most equity funds charge 1% if redeemed before 12 months. Long-term capital gains above ₹1.25 lakh are taxed at 12.5%. Short-term gains at 20%.

These numbers add up. On any meaningful portfolio, poorly timed exits can wipe out a year's outperformance.

The +3.3% lump-sum figure and +3.8% SIP figure both factor in exit loads and applicable capital gains tax at rebalance. What you see is what stays in your pocket — not a pre-tax number dressed up to look better.