Money is an imaginary concept! In itself, it has no value. It’s just a piece of paper or a number on your computer screen.

So why does everyone want it then?

Well, you don’t want money just for the sake of having it. You want money because of what it can get you. In other words, you want money because it lets you accomplish your goals.

You might want a new car or a new house, or you want your kids to go to a nice college. Whatever the goal is, you need money to accomplish it.

Suppose it’s your 3 yr olds first day in school and you wish to see him or her graduating from a top-tier college one day. So you start a monthly SIP in the hope that by the time your kid is ready for college, you will have built up enough savings that your kid doesn’t have to worry about the fees.

But how much you should save depends on the rate of return you are assuming on your investment. That begs the question – what is the appropriate rate of return for goal planning?

In this article, we talk about the most appropriate rate of return for goal planning that will maximize your chances of reaching your goals.

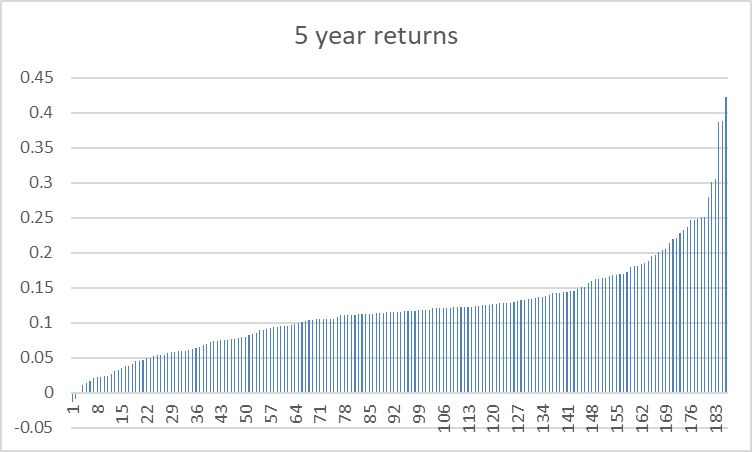

Making sense of the data

We ran through the past 20 years of Sensex data and arranged 186 sets of average 5-year rolling returns in the order of their returns.

The minimum and maximum returns (in the range of 5 years) were -1.5% Compound Annual Growth Rate (CAGR) and 42% CAGR, respectively. The average return stood at 12.1%.

The data below indicates that in any given 5-year period there is a 90% chance of making at least a 4.5% return. A 50% chance of securing a minimum of 11.6% return, and only about a 20% chance of enjoying returns exceeding 16.2%.

| Percentile | 5 Years Average Returns |

|---|---|

| 90th Percentile | Minimum 4.5% average return |

| 80th Percentile | Minimum 6.9% average return |

| 70th Percentile | Minimum 9.2% average return |

| 60th Percentile | Minimum 10.6% average return |

| 50th Percentile | Minimum 11.6% average return |

| 40th Percentile | Minimum 12.3% average return |

| 30th Percentile | Minimum 13.4% average return |

| 20th Percentile | Minimum 16.2% average return |

| 10th Percentile | Minimum 20.2% average return |

| 0th Percentile | Maximum 42.3% average return |

In fact, the chances of getting the 12% (average) or a higher return is 45%. That’s your chance of success.

So what’s the appropriate rate for you?

There is no one-size-fits-all when it comes to determining the appropriate expected rate of return for your goal. It depends on your personal risk tolerance and on the importance of your goal.

For example, saving for your kids’ education would ideally be far more important to you than say, saving for a car. Thus, if the goal is important to you, you would ideally want to keep the odds in your favor and select a rate of return with a slightly higher success rate, perhaps 70%, and hence use a lower rate of return in your calculations. In that case, the most appropriate rate of return for you would be 9.2% (refer to Table 1) instead of the average 12%.

The Next 5-Year Returns

Taking the discussion further, we analyzed whether the previous 5-year returns affect the next 5-year returns. In other words, if the markets have performed exceptionally well in the past 5 years, should you expect a lower-than-average return for the next 5 Years?

| Average – Next 5-Year Returns | Minimum – Next 5-Year Returns | Maximum – Next 5-Year Returns | |

|---|---|---|---|

| Previous 5 Years Returns > 20% | 8.5% | 2.4% | 12.3% |

| Previous 5 Years Returns between 15-20% | 11.4% | 5.0% | 17.0% |

| Previous 5 Years Returns between 10-15% | 11.8% | 3.1% | 18.2% |

| Previous 5 Years Returns between 5-10% | 10.1% | 1.1% | 18.9% |

| Previous 5 Years Returns < 5% | 11.2% | 6.0% | 13.9% |

The data indicates that only when the previous 5-year average returns are over 20%, the next 5-year average returns fall to 8.5%. In all other cases, the 5-year average return is within the narrow range of 10 to 12%. Therefore, when the markets have performed exceptionally well in the last 5 years, you should take a more conservative approach and lower your expectations accordingly.

Conclusion

In conclusion, planning your money for your goals is super important. You should never blindly guess how much extra money you’ll make. Look at the numbers, understand your goals, and make the most informed decision to make your dreams come true.

Thank You for Reading!

Related Posts

Why doing too much is holding back your returns

The ability to do nothing is so powerful for your portfolio Most investors believe that…

How to keep calm amid market volatility

Stay rooted in principles and don’t follow the herd Sir Isaac Newton is widely regarded…

Why We Built Gear 6 for Mutual Funds — And How It Works

Why We Built Gear 6A for Mutual Funds — And How It Works India’s mutual…

Smart Beta Strategies: What Investors Should Know Before Investing

Smart Beta Strategies: What Investors Should Know Before Investing As of August 2025, Indian mutual…